What are Anna Maria’s best options for lowering the giant tax bill her family faces this year?

What are Anna Maria’s best options for lowering the giant tax bill her family faces this year?

Article content

Q. My spouse earns $430,000 per year and has maxed out his Registered Retirement Savings Plan (RRSP) contributions and therefore is not eligible for further tax deductions. He has continued to contribute to the Employer Stock Purchase Plan (ESPP) which his employer matches. I earn $34,000 a year working part-time. I have accumulated an unused RRSP contribution amount of $45,000 from past years.

![]()

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman, and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

- Exclusive articles from Barbara Shecter, Joe O'Connor, Gabriel Friedman and others.

- Daily content from Financial Times, the world's leading global business publication.

- Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

- National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

- Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account

- Share your thoughts and join the conversation in the comments

- Enjoy additional articles per month

- Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Article content

On the home front, we have four children and some childcare expenses and medical expenses, as well as university tuition costs. What are our best options for lowering the giant tax owing that I fear we face this year? Could I buy RRSPs and receive a refund that might slightly offset our tax bill? Should we just pay the tax? Or is there something else we should be doing? —Thanks, Anna Maria

Article content

Article content

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Article content

FP Answers: Contributing to an RRSP will give you a tax deduction that can lower your taxable income and will usually result in tax savings. However, it may not always be the best idea in the long run, Anna Maria. RRSPs are most effective if you contribute in higher income years and withdraw in lower income years.

Article content

Given your income of $34,000, the tax savings would be minimal at around 20 per cent in most provinces. You also have childcare expenses you can deduct as the lower income spouse. The tax savings at the highest marginal tax bracket in some provinces are 50 per cent or more. Future withdrawals from your RRSP may end up getting taxed at much higher rates. If your spouse has a large RRSP that is maxed out every year, he can split future Registered Retirement Income Fund (RRIF) withdrawals with you once he is 65 years old, and your tax rate could be much higher in retirement.

Article content

Article content

Tax refunds can provide short-term cash flow, but timing when you deduct RRSP contributions is important. If you anticipate a future capital gain that will push up your income, an RRSP contribution may be more beneficial in a future year.

Article content

Article content

Beyond RRSPs, you should max out your Tax-Free Savings Accounts (TFSAs) annually. If you haven’t contributed to these accounts in the past you may have as much as $204,000 in contribution room between you and your spouse.

Article content

You should contribute to a Registered Education Savings Plan (RESP) to get the Canadian Education Savings Grant, which provides $500 in government grants for each $2,500 contributed per child. The funds also grow tax deferred, and withdrawals are taxable to the student.

Article content

If your TFSA and RESP accounts are maximized, you could consider debt repayment if you have debt. This may not save you tax, but it will save you interest expenses.

Article content

Your spouse cannot give you money to invest to avoid paying tax at their higher tax rate. There is a concept called attribution that prevents this. If your spouse gives you money to invest in a taxable account, the resulting income and capital gains get taxed back to you. That is, unless the money is loaned at the Canada Revenue Agency (CRA) prescribed rate, which is currently three per cent.

Sponsorizzato

Sponsorizzato

Sponsorizzato

Sponsorizzato

Pubblicità

Categorie

Leggi tutto

Watch: BBC journalist caught in travel chaos at Houston AirportTravellers across the US are facing unusually long lines at airports, as hundreds of Transportation Security Administration (TSA) agents have quit while others continue to miss paychecks and call out of work amid a partial government shutdown. BBC journalist Christal Hayes was returning home after her honeymoon and was caught in the...

Best Streaming Services for Kids in 2026What's the best kids streaming service overall?Netflix and Disney Plus may be the top choices in your household when it comes to kids' programming. The content libraries featured on each platform offer a diverse range of family-friendly TV shows and movies suitable for various age groups. Choosing our top pick from our list of best...

What is the U.S. military's capacity to carry out extended strikes in Iran?What is the U.S. military's capacity to carry out extended strikes in Iran? Seth Jones of the center for Strategic and International Studies talks about the U.S military's capacity to carry out extended strikes in Iran, and Iran's ability to retaliate. World What is the U.S....

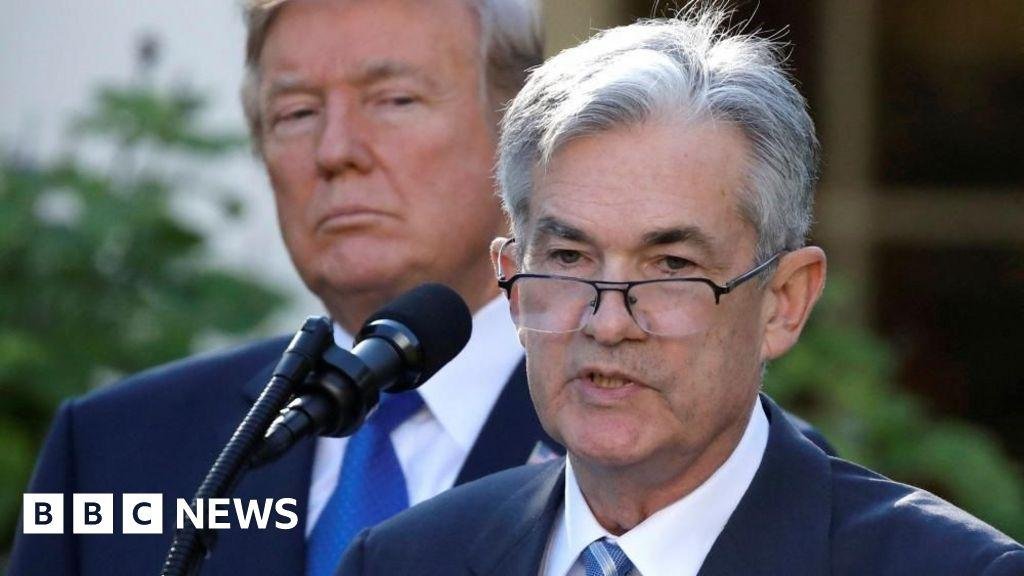

US justice department drops probe into Fed chairman Jerome Powell35 minutes agoJemma CrewBusiness reporter ReutersThe US justice department is dropping its investigation into the Federal Reserve chairman, Jerome Powell, over alleged building cost overruns.US Attorney Jeanine Pirro said instead there would be an internal investigation led by the central bank's inspector general.President Donald...

Police identify suspect in Rhode Island ice rink shootingGetty ImagesThe shooting happened at the Dennis M Lynch Arena in Pawtucket, about five miles (8km) north of the state capital, ProvidencePolice have identified the suspect in a shooting at a high school ice hockey game in Rhode Island that killed two people and injured three others.Pawtucket Police Chief Tina Goncalves said Robert Dorgan,...